Navigating Medicare can feel overwhelming, with multiple plan types, enrollment windows, and coverage options that affect healthcare costs for years to come. Working with a knowledgeable medicare advisor helps beneficiaries understand their options and select coverage that genuinely fits their health needs and budget. Understanding the basics of health insurance medicare supplement plans is the foundation of making an informed enrollment decision.

The Four Parts of Medicare Explained

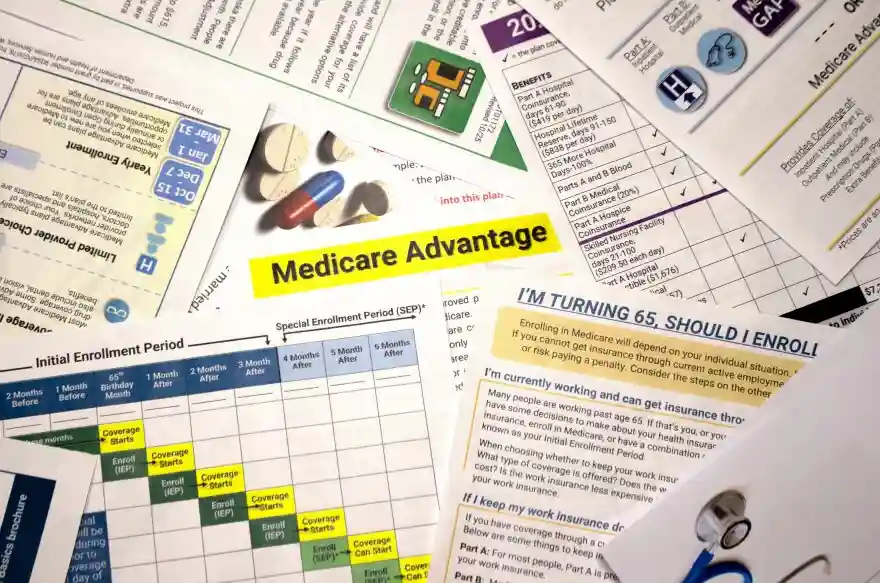

Medicare is organized into four distinct parts, each covering different aspects of healthcare. Part A covers inpatient hospital stays, skilled nursing facility care, hospice, and limited home health services, most beneficiaries receive Part A premium-free based on their work history. Part B covers outpatient medical services, doctor visits, preventive care, and durable medical equipment, and carries a standard monthly premium. Part C, known as Medicare Advantage, is an alternative delivery option offered through private insurers. Part D covers prescription drug costs. Understanding how these parts interact is essential before choosing supplemental coverage.

What Medicare Supplement Plans Cover

Original Medicare Parts A and B leave beneficiaries responsible for significant out-of-pocket costs, including deductibles, copayments, and the 20% coinsurance that Medicare does not cover on Part B services. The health insurance medicare supplement plans, also called Medigap policies, are sold by private insurance companies to fill these gaps. Depending on the plan letter selected, Medigap coverage can pay Part A and B deductibles, hospital coinsurance, skilled nursing facility coinsurance, and even limited foreign travel emergency coverage. Because benefits are standardized by the federal government, beneficiaries can compare plans from different insurers with confidence that the coverage is identical.

Medicare Advantage as an Alternative Approach

Medicare Advantage plans offer an alternative to original Medicare plus a Medigap supplement by bundling hospital, medical, and often drug coverage into a single plan administered by a private insurer. These plans frequently include additional benefits not available in original Medicare, such as dental, vision, hearing, and fitness programs. However, they typically operate within provider networks that restrict which doctors and hospitals members can use. Cost-sharing structures differ from original Medicare and Medigap combinations, making direct comparison essential before enrollment.

Critical Enrollment Periods Every Beneficiary Must Understand

Medicare enrollment is governed by specific windows that, if missed, can result in permanent late enrollment penalties or delayed coverage. The Initial Enrollment Period surrounds a beneficiary’s 65th birthday and represents the primary opportunity to enroll without penalty. Those who continue working and maintain employer coverage may qualify for a Special Enrollment Period when that coverage ends. The Annual Enrollment Period each fall allows beneficiaries to make changes to Medicare Advantage and Part D plans.

The Value of Working with a Medicare Specialist

The complexity of Medicare decisions makes professional guidance genuinely valuable for most beneficiaries. An independent medicare advisor reviews a client’s specific health situation, prescription drug needs, preferred providers, and financial constraints to recommend coverage options objectively. Unlike agents who represent a single carrier, independent advisors have access to multiple plan options and can present comparisons that help beneficiaries identify the combination that offers the best value.

Conclusion

Choosing Medicare coverage is one of the most consequential healthcare decisions most people make, with implications that affect access to care and out-of-pocket costs for the rest of their lives. Understanding the structure of Medicare, the role of supplement plans, and the importance of enrollment timing helps beneficiaries approach this decision with the clarity it deserves. Working with a qualified Medicare advisor ensures that the final coverage decision reflects a complete, accurate understanding of the available options and the individual’s specific circumstances.